Explore key trends in the Q2 2025 Fine Wine Market Report – from Trump’s proposed tariffs to Bordeaux En Primeur 2024, index performance, and standout wines like Chave Hermitage and Screaming Eagle. Discover where value and stability are emerging.

Executive summary

- Trump’s proposed tariffs dominated headlines, yet the delayed implementation gave markets breathing room.

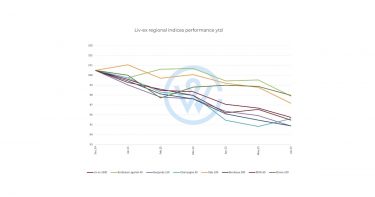

- The Liv-ex 100 index declined 3% in Q2 but showed signs of levelling off by quarter-end.

- Bordeaux En Primeur 2024 was met with weak demand driven by oversupply and collector preference for mature vintages.

- Regional performance diverged, with Bordeaux and Burgundy leading declines, while Champagne showed signs of stabilisation.

- Top-performing wines defied broader market trends, with double-digit gains from names like Chave Hermitage 2021, Château d’Yquem 2014, and Screaming Eagle 2012.

- Fine wine remains in a correction phase, but select names, regions, and vintages continue to offer compelling investment opportunities.

The trends that shaped the fine wine market

Global markets adjust as tariff volatility eases

President Trump’s revival of protectionist trade policies set the tone for global markets in Q2. From January to April, the average U.S. tariff rate on imported goods like cars, steel, and aluminium surged from 2.5% to a century-high 27%, before easing to 15.8% in June.

While the March tariff threat initially triggered sharp volatility, the fallout was relatively short-lived. Early April brought a brief dip into bear territory for the S&P 500 on tariff fears. But with policy pauses and stronger-than-expected earnings – 78% of S&P companies beat forecasts – investor confidence returned. Equities in Europe and Asia rallied as well, with the FTSE 100 testing new highs. Corporate investment, especially in AI, remained robust despite political and fiscal uncertainty.

This broader resilience helped buoy alternative assets like fine wine. While less liquid than stocks, fine wine saw continued interest from long-term investors. Crucially, there was no evidence of panic selling – a sign of confidence in the asset class’s underlying stability.

Telling signs of stability in the fine wine investment market

The pace of fine wine price declines slowed in the second half of the second quarter, although the market is not yet in full recovery mode. On average, fine wine prices as measured by the Liv-ex 100 index, dipped 3% in Q2 2025. The index has been in a freefall since September 2022, seeing only five minor upticks during this time. Meanwhile, the Liv-ex 50, which tracks the performance of the Bordeaux First Growth, has been in a consistent decline during the last 33 months.

Still, the recent falls have been less pronounced, and prices for many of the index component wines have maintained their new levels without falling further. The market seems to be adjusting to the new environment, with participants showing greater acceptance of the status quo and reduced sensitivity to geopolitical noise. In Q2, demand even began to resurface, particularly from Asia, which has been notoriously quiet, and the U.S., which had initially retreated due to tariff fears.

Muted demand for Bordeaux En Primeur 2024 as market shifts for mature wines

With the market still absorbing past vintages and saturation setting in, enthusiasm for Bordeaux En Primeur 2024 was notably subdued. Despite reduced release prices, the wines often failed to offer compelling quality or value when compared to older vintages readily available on the secondary market.

Bordeaux’s structural challenges persist. Negociants remain overstocked and weighed down by rising bank interest, while many merchants lack the appetite or capital to buy for stock. Meanwhile, the once-crucial Chinese market remains largely dormant.

This muted campaign reflects a broader shift in buyer behaviour. Demand has tilted decisively toward mature wines with a track record of quality and drinkability. While the short-term appeal of buying young futures has faded for now, Bordeaux’s reputation for ageability and long-term value endures.

Fine wine vs mainstream markets in H1 2025

While mainstream equity markets swung between bear and bull phases in Q2, the fine wine market charted a notably more stable path. Fine wine prices declined modestly over the period, but without the sharp drops or rallies seen in the S&P 500, Dow Jones Industrial, or FTSE 100. The contrast, seen in the chart above, reinforces fine wine’s reputation as a lower-volatility asset during times of heightened macroeconomic and geopolitical uncertainty.

Importantly, this steady decline was not marked by panic selling or dramatic shifts. This reflects the market’s structural differences: lower liquidity, longer holding periods, and a collector-investor base that prioritises wealth preservation over short-term trading.

Moreover, beneath the surface, outliers and outperformers remain. Read on to discover where relative value has emerged, and which regions and producers have shown resilience – or even strength – so far this year.

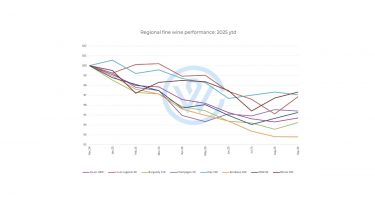

Regional fine wine performance: year-to-date trends

The first half of 2025 has revealed consistent pressure across nearly all fine wine indices, with no region posting growth year-to-date. Yet the degree of decline varies.

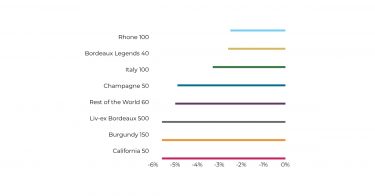

Bordeaux and Burgundy lead declines (-5.6%)

Both the Liv-ex Bordeaux 500 and Burgundy 150 have posted the steepest year-to-date losses among the major indices, each down 5.6%. For Bordeaux, this reflects tepid interest in younger vintages and a sluggish En Primeur campaign, coupled with a lack of support from Asia. Burgundy continues to correct from previous pricing spikes, as buyers recalibrate in search of better relative value.

Auction results defy the indices

While Bordeaux and Burgundy’s regional indices posted year-to-date declines of -5.6%, recent auction results tell a different story at the very top end of the market.

In June 2025, Christie’s held a landmark sale of the personal wine collection of billionaire collector Bill Koch, generating a record-breaking $28.8 million over three days. The sale drew global participation and intense bidding across 1,500 lots, each of which was sold. The standout was a 1999 Romanée-Conti Methuselah, which fetched an eye-catching $275,000.

The collection featured rare Bordeaux and Burgundy – the very categories currently under pressure in secondary market indices – yet buyer appetite was strong, and prices exceeded estimates across multiple lots.

Champagne shows relative stability

The Champagne 50 has held up better than most, down just 4.9% year-to-date, and was the only region to show positive month-on-month growth in June (+0.8%). While the broader category has cooled after a strong run, interest in top names remains, especially among collectors focused on prestige and scarcity. Indeed, many of Champagne’s top brands now represent the best entry point into the region in years. Prices have stabilised, and there are signs they will not fall any further, but might start to rise again.

Broader weakness across other regions

- Rest of the World 60 is down 5.0%, showing soft demand beyond the mainstay regions.

- California 50, also down 5.6%, mirrors this trend and highlights ongoing sensitivity to U.S. economic and tariff concerns.

- Italy 100 has dropped 3.3%, suggesting a more measured pullback, consistent with the region’s reputation for offering value and dependable quality.

- Bordeaux Legends 40 and Rhone 100 are holding up best, with declines of only 2.6% and 2.5% respectively. This speaks to market confidence in mature Bordeaux and Rhône’s reputation for steady, value-driven performance.

As the fine wine market works through broader corrections, defensive regions – particularly Rhône and mature Bordeaux – are outperforming, while Burgundy and California remain under pressure. Champagne’s recent bounce may signal early signs of selective recovery. For investors, opportunities may lie in regions demonstrating resilience rather than those still working through valuation resets.

The best-performing wines so far this year

Despite broad declines across regional indices, a select group of wines delivered standout returns in H1 2025, highlighting the importance of producer reputation, scarcity, and vintage specificity in fine wine performance.

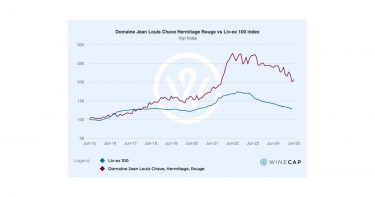

The Rhône leads driven by Chave

The top-performing wine was Domaine Jean Louis Chave’s 2021 Hermitage Rouge, which rose +36.8% in the first half of the year. This outperformance stands in stark contrast to the overall Rhône 100 index, which declined 2.5%. Over the last decade, prices for the brand are up 127% (compare its performance to other market benchmarks on Wine Track).

Château d’Yquem 2014 and Château Suduiraut 2016 returned 25.7% and 23.9% respectively, bucking the downward trend in Sauternes. On a brand level, Yquem has risen 7% in the last six months and 3% in Q2; Suduiraut is up 11% in H1 2025. These results signal renewed collector appetite for premium dessert wines – particularly in top vintages where quality and longevity are indisputable – yet prices remain relatively low.

Prestige investment opportunities in Napa and Champagne

The California 50 index fell 5.6%, but iconic Napa cult wine Screaming Eagle 2012 rose 24.4%, affirming the strength of globally recognised, ultra-luxury labels. Indeed, average prices for the brand rose 5% in H1 2025. Similarly, Pol Roger Sir Winston Churchill 2015 posted a 24.4% gain, demonstrating that top-tier Champagne continues to attract collectors even as the Champagne 50 index overall declined.

Burgundy and Tuscany standouts reinforce blue-chip strategies

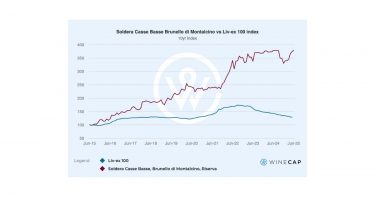

Despite Burgundy’s broader correction, DRC’s La Tâche 2020 and Clos de Tart 2013 delivered 24.5% and 18.1% returns respectively. These names remain benchmarks of rarity and prestige. Meanwhile, Soldera Case Basse 2018 gained 14.3%, pointing to sustained momentum behind top Italian producers. In Q2 alone, prices for the Tuscan premium brand are up 11%; in H1, 16%.

Investor takeaways

- Market-wide declines don’t mean universal losses. Select wines not only held value but also delivered double-digit returns.

- Rarity and recognisability remain key drivers. Names like Chave, Yquem, Screaming Eagle, and DRC continue to offer portfolio resilience.

- Smart vintage selection pays. Wines from underappreciated years – like Canon 2014 – produced outsized gains relative to their pricing base.

- Dessert wines are back on the radar. Contrarian plays in Sauternes may offer continued upside in H2 2025.

Brands to watch

Signs of a Champagne revival

After being the fine wine market’s standout performer in 2022, Champagne experienced one of the sharpest pullbacks during the broader market correction of 2023–2024. However, signals suggest the tide may now be turning again.

From peak to pause: A market in transition

Prices across the Champagne sector have fallen significantly from their highs, but the sell-off appears to have run its course. June marked a notable shift: Champagne was the first regional index to post positive month-on-month growth, rising +0.8%, a potential inflexion point after months of stagnation.

More importantly, price stability has returned. The sector’s recent performance suggests we may be entering a new phase of the Champagne investment cycle, where prices consolidate before a potential recovery.

Market data signals stabilisation

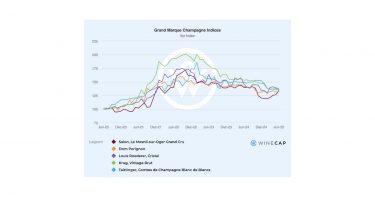

To test this trend, we analysed the 10 most recent vintages of the five most-searched “Grand Marque” Champagnes:

- Dom Pérignon: 2015, 2014, 2012, 2010, 2009, 2008, 2006, 2005, 2004, 2003

- Cristal: 2016, 2015, 2014, 2013, 2012, 2009, 2008, 2007, 2006, 2005

- Salon Le Mesnil: 2013, 2012, 2007, 2006, 2004, 2002, 1999, 1997, 1996, 1995

- Krug Vintage: 2011, 2008, 2006, 2004, 2003, 2002, 2000, 1998, 1996, 1995

- Taittinger Comtes de Champagne: 2013, 2012, 2011, 2008, 2007, 2006, 2005, 2004, 2002, 2000

Of these 50 individual wines,

- 43 have resisted their price declines,

- 40 have remained stable for at least six months,

- the indexes aggregating their vintages confirm this plateau.

Notably, Dom Pérignon has shown the earliest and most sustained stabilisation, with its index bottoming out in November 2024. Krug Vintage and Taittinger Comtes de Champagne are the most recent to enter this stable phase, suggesting broader alignment across the category.

A new phase for Champagne?

This pattern of index symmetry and brand-level stabilisation is a clear signal that Champagne may be transitioning from correction to consolidation. Investor sentiment appears to be catching up to underlying fundamentals, with many of Champagne’s leading brands now offering compelling re-entry points. Liv-ex market share data supports this trend:year-to-date, Champagne has taken 12.4% of the market by value, up from an annual 2024 average of 11.8%, signalling that demand is returning.

If this trend holds, Champagne could become one of the first major regions to re-enter positive growth territory, supported by brand power, vintage scarcity, and collector loyalty.

Q3 2025 market outlook: A pause before the pulse?

The third quarter – traditionally the quietest in the fine wine calendar – arrives amid a tentative calm. Following the volatility of Q2, Q3 is shaping up to be more subdued but not without potential catalysts.

Tariff watch

President Trump’s planned tariffs, originally slated for Q2, have now been delayed until August 1st. Markets have so far responded with a muted shrug, suggesting either tariff fatigue or confidence that negotiations may temper the final impact. But the uncertainty remains a live wire: should enforcement proceed, volatility could resurface late in the quarter. For now, however, investors appear cautiously indifferent.

La Place de Bordeaux’s autumn window

With the Bordeaux 2024 En Primeur campaign having underwhelmed, attention now turns to La Place de Bordeaux’s autumn campaign. This presents a rare chance for standout producers from around the world to seize attention, particularly those releasing back vintages or special bottlings. A well-priced, tightly-curated campaign could reignite interest and provide pockets of momentum in an otherwise quiet market.

Rest of the World builds buzz

As traditional strongholds like Bordeaux and Burgundy continue to correct or stagnate, Rest of the World wines are beginning to command more attention. California, Tuscany, and Rhône producers featured prominently among H1’s top performers, and collectors may increasingly look to these regions for value, scarcity, and differentiation in the second half of the year.

A stable market… but will it rise?

Fine wine’s reputation for stability held firm in H1, avoiding the sharp swings seen in equities. The question now is whether this stability will give way to price appreciation. While some wines are poised to rise, we expect the broader market to remain sluggish through the summer. Liquidity typically thins in July and August, and the broader mood is unlikely to shift meaningfully until September.

What to watch

- Tariff developments post-August 1st

- Autumn releases on La Place, especially non-Bordeaux

- Top Champagne brands starting to rise in value

- Collector appetite for emerging regional stars

- Signs of rotation from defensive to opportunistic buying behaviour

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.