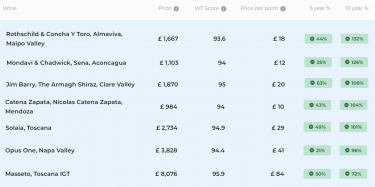

- The fine wine market is diversifying, with Argentina and Switzerland making new entries in the 2023 Liv-ex Classification.

- Bordeaux’s influence is waning, now accounting for less than 30% of wines in the classification, while other regions like Champagne rise in prominence.

- Internal shifts in Burgundy indicate changing buying preferences, driven by the search for value and stock.

The Liv-ex Classification is a ranking of the world’s leading fine wine labels, based solely on their price. The classification takes into account minimum levels of activity and number of vintages traded over one year to present a more accurate picture of the market today. Like the 1855 Bordeaux Classification, the wines are divided into five tiers (price bands).

The 2023 edition featured 296 wines from nine countries. It presented a broad overview of the state of the secondary market – what is trading, and at what price levels. As the market continues to evolve, we break down four key trends from the 2023 Liv-ex classification.

Continued expansion in the world of fine wine

While the number of wines that qualified for inclusion in the 2023 rankings was lower than in the previous 2021 edition (349) due to changes in the methodology, the fine wine investment market has continued to diversify.

Argentina re-entered the rankings with five wines compared to having just one in 2019. Switzerland also joined the classification for the first time with Gantenbein Pinot Noir. Meanwhile, Spain and Chile saw 40% and 100% respective increases in the number of wines entering.

Regional diversity was particularly noticeable in the second-lowest priced 4th tier (£456-£637 per 12×75), which featured wines from France (24), Italy (16), Portugal (3), Australia (2), Spain (1), the USA (1), and Argentina (1).

Bordeaux among global competitors

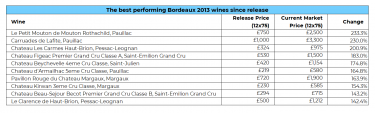

It is no secret that Bordeaux’s dominance in the fine wine investment market has been fading since its glory days in 2009-2010. The continued broadening of the market has meant that the region has become one of many players, accounting for under 30% of the wines in the 2023 classification.

This has been further aided by its mediocre price performance relative to other regions. The Bordeaux 500 index has risen just 2.9% over the last two years, compared to a 19% move for its parental Liv-ex 1000 index, and a 36.7% increase for Champagne, which has been the best performer. All considered, Liv-ex wrote that ‘this pattern may well continue in future editions’ as new entrants challenge Bordeaux’s monopoly.

While Bordeaux’s influence wanes, other regions like Champagne are capturing the limelight.

The stellar rise of Champagne prices

Champagne has experienced a significant price surge in recent years, which has been reflected in the global rankings.

The majority of Champagnes (10) in the classification entered the first tier – wines priced above £3,641 per 12×75. The remaining 12 were split between tier 2 (£1,002-£3,640) and tier 3 (£638-£1,001). There were no Champagnes in tiers 4 and 5 (wines below £1,000 per case).

The most expensive Champagne was Jacques Selosse Millésime, with an average trade price of £32,516 per case, followed by Krug’s Clos d’Ambonnay (£30,426) and Clos du Mesnil (£17,509). The latter has risen 105% in value over the last five years.

On average, Champagne prices are up 62.8% during this time. They peaked in October 2022, following a year and a half of steady ascent. Since then, the Liv-ex Champagne 50 index has entered a corrective phase – but not significant enough to change the region’s trajectory. Sustained demand has been further buoying its performance.

Internal reshuffling in Burgundy

Burgundy, home to the most expensive wines in the rankings, has been undergoing an internal shift. New entrants have replaced many of the labels in previous editions, signalling changes in buying preferences.

Heightened demand for the region in 2022 led buyers to explore different wines within Burgundy, seeking both value and stock availability. Some of the new entrants in the 2023 classification include Prieuré Roch Ladoix Le Clou Rouge, Domaine Louis Jadot Gevrey-Chambertin Premier Cru Clos Saint-Jacques and Domaine Trapet Père et Fils Latricières-Chambertin Grand Cru.

Interestingly, while these new labels have entered the ranking, they seem to have replaced older, perhaps less active, Burgundy labels. Indeed, the overall proportion of Burgundy wines in the classification has remained steady, even as specific labels fall in and out of favour.

As new players emerge and existing ones adapt, one thing is clear: the fine wine market will continue to diversify and evolve, promising a fascinating future for everyone involved.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.