- Fine wine investment differs significantly from traditional markets because supply diminishes with time.

- Holding periods determine whether an investor benefits from liquidity windows, maturity or scarcity premiums.

- Investors should not expect uniform results across all wines or timeframes.

When it comes to fine wine investment, most discussions focus on the what: which wines, which vintages, which regions. Equally critical, but less often addressed, is the when: how long you hold your investment.

Holding periods can dramatically shape your returns, mitigate risks, and define your overall strategy. Unlike equities or bonds, fine wine is both a physical asset and a cultural commodity, with unique cycles of demand and consumption. Understanding how time interacts with these cycles is essential for building a resilient portfolio.

Why holding periods matter in wine investment

Fine wine investment differs from traditional markets in one key respect: supply diminishes over time. Bottles are uncorked and consumed, which means that scarcity increases naturally as years pass. At the same time, the wines themselves evolve in bottle, often improving in complexity and desirability. This dual dynamic of shrinking availability and increasing quality drives long-term price appreciation.

However, investors cannot expect uniform results across all wines or timeframes. Some wines appreciate rapidly within a few years, while others demand decades of patience. Holding periods determine whether an investor benefits from:

- Liquidity windows – when supply and demand align to create strong secondary market interest.

- Maturity premiums – when wines are at or approaching their drinking peak.

- Scarcity premiums – when older vintages are nearly impossible to source.

Short-term wine investment holds (1–3 years): Potential high gains?

Short-term holding in fine wine is less common but not without opportunity. Investors might target wines with clear catalysts for appreciation in the near future:

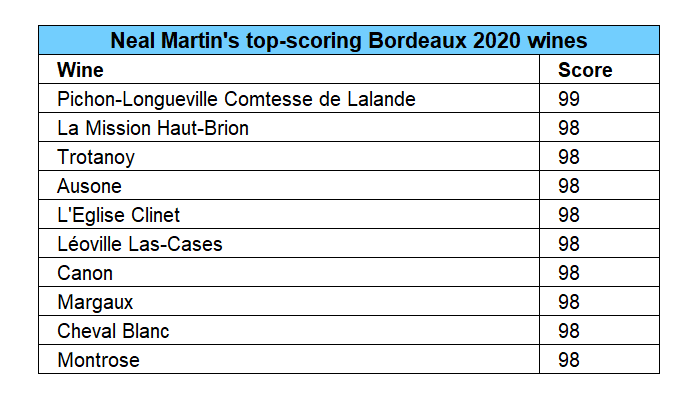

- Critical acclaim: A 100-point score from leading critics such as Robert Parker, Neal Martin, or Antonio Galloni can trigger immediate demand.

- Market cycles and estate events: Certain vintages or regions may benefit from renewed attention during En Primeur campaigns or La Place de Bordeaux releases. Similarly, external factors such as a change of ownership, the passing of a renowned winemaker, or a significant new investment in the estate can act as a catalyst. These events often lead to brand repositioning and higher release prices for new vintages, which in turn push up the value of older vintages as buyers seek relative value.

- Macro-drivers: Currency fluctuations, tariff shifts or geopolitical events can create short-term arbitrage opportunities.

That said, short-term holds may carry higher volatility. Transaction costs – storage, insurance, brokerage fees – also eat more heavily into returns when compounded over only a few years. As a result, short-term trading tends to suit sophisticated investors with high market awareness rather than long-term collectors.

Medium-term wine investment holds (5–10 years): The sweet spot?

The medium-term horizon is often considered the sweet spot for many wine investors. This is when:

- Wines mature: Many Bordeaux, Burgundy, and Champagne houses see optimal secondary market demand when their wines are 5–10 years post-vintage. At this stage, they have begun to show character but remain relatively youthful, making them appealing to both collectors and drinkers.

- Supply drops: The first wave of consumption removes weaker hands from the market, while professional storage ensures the surviving bottles command a premium.

- Liquidity is strong: Buyers – both private and institutional – seek wines that are ready-to-drink but still have substantial cellaring potential.

This period allows investors to capture meaningful appreciation without committing to decades of illiquidity. For many, the medium-term strategy provides a balance of growth potential and portfolio flexibility.

Long-term wine investment holds (10–20+ years): Scarcity and compounding value?

For truly iconic wines, long-term holding unlocks the greatest rewards. Scarcity compounds dramatically after 15–20 years, and mature bottles often become the centrepiece of collectors’ cellars. Wines that especially benefit from this approach include:

- First Growth Bordeaux: Château Lafite, Latour, and Margaux often reach their full secondary market potential decades after release.

- Grand Cru Burgundy: Producers like Domaine de la Romanée-Conti or Armand Rousseau are prized for aged expressions, which are scarce even at release.

- Prestige Champagne: Top cuvées such as Krug or Salon are often held back by maisons themselves, releasing older vintages at a premium.

The trade-off is clear: long-term holding requires patience, optimal storage, and careful insurance. Illiquidity can become an issue if capital is needed suddenly. However, for investors with a multi-decade outlook, these holds can deliver extraordinary compounding returns – often well outperforming traditional assets.

Factors that impact value over time

Not all wines follow the same trajectory. Determining how long to hold depends on a mix of factors:

- Region and style

- Bordeaux and Napa Cabernet: typically longer arcs, rewarding 10–20+ years.

- Burgundy Pinot Noir: often peaks earlier (7–15 years), though the best can go much longer.

- Champagne: prestige cuvées benefit from extended ageing, while non-vintage wines are less suited to investment.

- Producer reputation

Iconic names command steady demand across all stages, while lesser-known producers may see sharper peaks tied to critical acclaim. - Vintage quality

Strong vintages (e.g., Bordeaux 2000, Champagne 2008) often sustain demand longer, while weaker vintages may peak quickly. - Critic scores and re-releases

A re-rating or late-release program can extend or shift the ideal holding window. - Market conditions

Global economic health, currency exchange rates, and tariffs can all affect when it’s most profitable to sell.

Risks of mistimed holding

Holding periods are not without risk. Selling too early can mean missing out on peak premiums. Selling too late risks encountering diminishing returns as wines pass their drinking window. Additionally, improper storage can compromise value, no matter the holding period. There are also liquidity risks: Even top wines may face temporary illiquidity in weak markets.

This is why professional portfolio management and exit planning are critical in fine wine investment.

Practical guidance for wine investors

- Diversify holding periods: Mix short, medium, and long-term positions across your portfolio. This smooths out returns and provides liquidity when needed.

- Match horizon to goals: If you expect to need capital in five years, avoid exclusively long-term wines.

- Work with data: Tools like Wine Track can help identify optimal exit windows by tracking price curves and critic sentiment.

- Reassess regularly: Market conditions evolve. A wine planned for long-term holding may benefit from earlier exit if demand spikes unexpectedly.

In fine wine investment, holding periods are the mechanism by which wine transforms from a consumable product into an appreciating asset. Short-term traders may profit from timing and market-driven gains, medium-term investors enjoy liquidity and strong demand, and long-term holders benefit from scarcity-driven premiums.

The best approach often combines all three, balancing risk and opportunity across different time horizons. With the right strategy, time becomes your most powerful ally – quietly compounding value as the bottles rest in the cellar.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.

*UK

*UK *US

*US *UK

*UK *US

*US